Floating Memories: My Three Meetings with "Chan Zhong Shuo Chan" Li Biao

Author: Gu Weiling

Source: Gu Weiling's Blog (Sina)

Published: September 2012

It has been exactly one year since I opened my blog on September 10 of last year. On this day still worth commemorating, what should I write? Thinking about how part of my motivation for starting a blog came from the inspiration of Li Biao's "Chan Zhong Shuo Chan," and considering that I met Li Biao three times, during which he taught me many things that benefited me immensely, I wanted to use this blog post to recall my three conversations with "Chan Zhong Shuo Chan" blogger Li Biao. This is both a review of history and my tribute to Li Biao.

Since Li Biao is a sensitive figure and our conversations touched on sensitive topics, this post may provoke some controversy. But let me state: all the events I describe have already become history, and this history already has its publicly known conclusions. We should regard it with equanimity.

I recall that around the end of 1998, I was working as an operator at an institution. I was independently running a project but was short on capital and needed to find a partner. At that time, many private institutions wanted to run projects independently but lacked sufficient capital and social resources, so inter-institutional cooperation was very common — a form of complementary advantage.

Through a friend's introduction, I met Li Biao. The meeting was at the Kempinski Hotel coffee shop in Beijing. Two people came from their side: one wore glasses, had a square face, and looked affable; the other was handsome but appeared quite aloof. My friend introduced them: the one with glasses was Li Biao, and the other was Tang Fan.

I hadn't heard of either of them before. Through brief pleasantries, I discovered they knew many people in the circle — various major institutions and big players I casually mentioned turned out to be contacts of theirs. We quickly got down to business. They said they had several hundred million in capital and were looking for good projects. That day they asked me many questions about the project — the theme, margin deposits, cooperation models, and so on. Tang Fan did most of the talking, while Li Biao said relatively little.

At the time, this meeting was quite ordinary for me. To find project partners, I had met many institutions and big players before and since, so I didn't regard them with any special attention. But later I learned that these two were far from simple in the stock market and had pulled off several market-shaking feats. For various reasons, I ultimately did not partner with them.

Time flew to early January 2000. The internet and tech concept stocks were all the rage, and strong market-maker stocks were in their heyday. My project had hit a snag — a partner had to withdraw nearly 100 million yuan from the stock market for special reasons. Time was extremely tight. If a buyer couldn't be found quickly, the consequences would be dire. So I embarked once again on a capital-hunting journey.

A "capital broker" friend with extensive connections said there was someone who operated Yi'an Technology and should have a solution. He arranged an introduction. Yi'an Technology was one of the biggest bull stocks at the time, having risen from just over 4 yuan to over 40 yuan — more than a tenfold increase (it later reached 126 yuan, but that's another story).

I was genuinely curious to meet this bull stock's operator. When I saw him, he looked familiar, and I quickly recalled — it was Li Biao. With my reminder, Li Biao recognized me too. We were at least old acquaintances, so this time our conversation went much deeper.

The topic naturally began with Yi'an Technology. Li Biao gave me a rough overview of his work on Yi'an Technology. He said the project had been entrusted by Luo Cheng, Yi'an Technology's CEO, to their team (later, CSRC documents on Yi'an Technology mentioned operators Li Biao, Tang Fan, and others by name). He was responsible for accumulating shares and the first wave of price increase. Now his part was done and he'd handed operations to someone else, though he still closely followed the daily price action.

On the topic of accumulation, Li Biao said the key to success was secrecy, which required considerable ingenuity. He said many people in the circle knew him — the moment he appeared at any brokerage office, the branch manager would monitor his accounts. To avoid surveillance, he had to open accounts at remote, unfamiliar brokerage branches.

After opening accounts, to deceive the brokerage staff, he would first go fully long on other stocks, then completely sell them out — repeating this several times. The brokerage staff, seeing he seemed like a poor trader, stopped paying attention. Then, when he went all-in on Yi'an Technology, no one took notice. Once accumulation was complete, he would transfer custody. This way he avoided being tracked.

Of course, even this couldn't escape the threat of "rat nests" (insider piggyback traders). These rat nests didn't come from information leaks on his part but from Yi'an Technology's own senior management. CEO Luo Cheng had entrusted Li Biao with the operation, and his inner circle of executives couldn't possibly not know. Luo Cheng also tacitly allowed executives to profit from it. So when Li Biao began accumulating, these executives and their extended networks simultaneously started buying, hoping to piggyback for big profits.

The executives thought Li Biao didn't know about these rat nests, but Li Biao was no fool — of course he knew. But he couldn't tolerate their existence. Under his agreement with Luo Cheng, Li Biao's compensation came from the project's eventual profits — either in cash or by splitting Yi'an Technology's base position. If rat nests ate up the base position, what profit was left for Li Biao?

After finishing the external accumulation, Li Biao began hunting the rat nests. But flushing them out was no easy task. The most decisive technique would normally be for the listed company to release major negative news — but this was unavailable to Li Biao, since the insider-trading executives knew even more about the company's secrets than he did.

Even if Yi'an Technology had some major negative news (which it didn't), at best Li Biao and the executives would learn of it simultaneously. He couldn't possibly use such news as a weapon against them without their knowledge. So the battleground between Li Biao and the executives was definitively not at the inside-information level. He had to find a better method.

Li Biao's enemy was not some outsider but his own "employer" — a truly remarkable scene. So how could he defeat his employer? Li Biao told me he intimately understood the executives' psychology: first, they didn't understand stocks but pretended they did; second, they were all extremely greedy and unwilling to accept even small losses; third, they believed they could control the situation. So to deal with them, he'd need a combination of tactics.

One day, he went to Luo Cheng's office and, deliberately in front of several vice presidents, loudly complained that Yi'an Technology's float was "dirty." He announced he needed to do a thorough washout — otherwise he couldn't continue. They feigned ignorance and asked how. Li Biao said he needed to smash the price down more than 30% and leave it at the bottom for six months to completely drive out the rat nests.

Li Biao knew Luo Cheng's people probably wouldn't believe him at first — these people didn't understand stocks, and you couldn't scare them with a sentence or two. But if Yi'an Technology's price actually broke down technically, the executives would get frightened. They'd take Li Biao's alarming words at face value, assuming the stock really was going to drop 30%. Better to flee now and re-enter later at a lower price or just before the next push-up — wouldn't that be smarter?

In the following days, Li Biao actually created a breakdown pattern in Yi'an Technology's chart. His technique was masterful: on one hand, spreading disinformation among the executives; on the other, engineering fake breakdowns in the stock price. Through this combination of counter-intelligence and deceptive charting, the executives' rat nests truly began a panic exodus. Li Biao, using secret accounts, absorbed every last share they dumped.

Li Biao described this episode in "Chan Zhong Shuo Chan," in Teaching You to Trade Stocks 87: Anecdotes of Playing with Market Makers 4:

"In this case, the rat nests started scrambling even before I'd made a move. So the task ahead was formidable: first, acquire enough shares; second, keep costs low; third, flush out the rat nests; and finally, do it all in limited time. By any measure, this was a mission impossible.

First, at a major resistance level, I held the line and absorbed all the shares from trapped sellers. Rat nests don't take on trapped sellers' shares — neither do small-time players. Then I kept making false breakouts at that position. At a strong resistance level, most people won't throw everything at breaking through. The repeated false breakouts made every technical trader hand over their chips. But at this point, what I'd bought was at the highest cost — everyone else's cost was lower except the historically trapped positions.

At this point, basically all the money was spent, with a little remaining. There was a type of intraday margin requiring same-day settlement. Using the remaining funds, I borrowed this margin. That day I bought ferociously — by morning all the cash plus margin was fully deployed. Because of the numerous previous false breakouts, nobody paid attention when it actually broke through — exactly the effect I needed.

In the afternoon, the position had to be closed. Repeated negotiations about deferral — answer: no. With great apparent anguish, I began the closing operation. Like a waterfall, prices plunged. Morning purchases were dumped at a loss, ending a 'tragic' trading day. The price crashed through the previously held platform. After close, rumors spread everywhere of someone being trapped and facing debt collection.

The next day, all the rat nests, all the insiders, stampeded for the exits. The third day, the same.

Meanwhile, from N remote locations, all the selling was absorbed into an anonymous pocket. Everyone who escaped was celebrating, because on the fourth day the stock still opened with a massive gap down."

After this thorough washout, Li Biao told me the final control rate of Yi'an Technology reached above 95%!

Of course, having flushed out the executives' rat nests, Li Biao understood that if things stopped here, he'd be in trouble. Once Yi'an Technology's price eventually rose and the executives were completely left behind, they would surely resent him. Li Biao said he was the kind of person who liked to leave things clean and flawless on the surface. So he deployed one more stratagem. Just before the major price run-up (a plan only he knew), he pretended to give the executives a "friendly tip."

He went to Luo Cheng's office and, in front of several confidants, chatted about other matters. Just as the meeting was wrapping up, he suddenly muttered to himself as if in passing: "If you're going to buy, buy now — once this train leaves, it's gone." I asked Li Biao: "Did those executives buy?" He laughed: "They probably thought I was joking. Besides, the washout had temporarily scared them witless — nobody dared buy right away. And anyway, all the shares were in my hands — even if they wanted to buy, there was barely anything to get. By telling them this, I was making clear that I hadn't forgotten to inform them before the run-up. Whether they bought or not was no longer my concern."

As the saying goes, "The real skill is off the board." Market-making is normally about capital firepower, but this was the first time I saw Li Biao deploy not capital strength but psychological warfare to control the situation — truly eye-opening. But his psychological warfare tactics didn't end there. The best was yet to come...

I asked Li Biao what stage Yi'an Technology was at now — whether he planned to push higher or distribute. He said distribution had already begun. So we discussed distribution techniques.

Though the market-maker era is long past, many investors still don't understand how market makers actually operated. Many stock commentators who never ran a book and never even met a real market maker wrote volumes of books like "Cracking the Market Maker Code," "Dancing with the Maker," and "Defeating the Market Maker" based purely on imagination — deeply misleading retail investors.

For instance, many say the distribution technique is "pump and dump," but few understand what this actually means in practice. Most people imagine the maker pushes the price to target, then starts dumping from the top — the "crash distribution method." This sounds logical but is miles from reality; the vast majority of market makers don't use the crash method.

The problem with "crash distribution" is that when the maker starts selling, the stock chart immediately deteriorates — topping patterns form, platforms break down. When the chart turns ugly, external buying dries up while selling floods in. With buy-sell imbalance, forced distribution triggers cascading selling. The maker may barely have distributed before the stock craters.

So the great majority of makers use the "pump-while-distributing" method — gradually selling while pushing the price higher. By the time the price peaks, most shares have been sold; the remainder can be dumped using the crash method. This yields a much higher average exit price and greater profit.

Before meeting Li Biao, I was already thoroughly familiar with the pump-while-distributing method but found it difficult to execute optimally. Two practical issues had always troubled me: what pace and pattern of price increase yields the best distribution results; and how to handle large buy orders that occasionally appear during the run-up.

Li Biao's view on the first question: during distribution, the chart pattern must be kept very clean and regular. He preferred platform-step increases — pushing up a segment, then consolidating in a small platform while keeping the price from falling, then pushing up again, then another platform, repeating. During the first couple of push-ups, buying would be hesitant. But once investors saw the stock moving in a regular pattern, they'd lose their fear. Especially after each platform breakout, buying would grow increasingly heavy, allowing the maker to distribute during the advance.

Keeping the platform flat was critical — it wouldn't scare off buyers or trigger selling. External buy and sell orders could reach self-equilibrium, requiring no maker intervention. Many less skilled makers could distribute during the push-up but had to keep buying during the platform phase to maintain it, eating back what they'd sold — defeating the purpose. The problem: their platforms weren't done right — either the price sagged, or the platform dragged on so long it killed all momentum.

Li Biao said the intraday time-share chart also needed clean, regular patterns during distribution. The basic principle: keep the line tidy — no haphazard moves. He loved using the Cantonese expression "goo-ling-gwai-gwai" (weird and tricky) — don't use any weird and tricky tactics during the run-up. Later, reading his "Chan Zhong Shuo Chan" concept of "trend tends toward perfection," I suspect it conveyed the same idea.

Li Biao said he only set an initial target distribution price. How high the stock would ultimately go during distribution depended on how the process unfolded. He once operated a stock, pumping and distributing simultaneously, and when the price hit its peak, suddenly found he had no shares left. After his exit, the stock actually continued rising on its own for a while. He said: that's the effect of doing it well — nobody can tell the maker has left. The trend stays beautiful and the upward momentum persists.

On the second question — large buy orders — Li Biao was emphatic: "When you see big buyers, you must give them shares! These large orders come unpredictably — sometimes appearing suddenly, but more often nowhere to be found. If you don't fill them, you may not find buyers for many days." As for whether these big buyers become adversarial (selling pressure the next day), Li Biao was unconcerned: all distributed shares could potentially become adversarial — if a maker feared that, they'd never distribute at all.

Then Li Biao made a point that transcended mere chart manipulation: many makers fail at distribution not because of chart technique but because they don't understand the full operational cycle. Most heads-down operators focus on the chart — engineering fake signals — with poor results. "The key to distribution is attracting external buying," he said. "Chart manipulation is only one method among many." I asked what better methods existed. He said: "During distribution, you absolutely must publicize! Broadcast everywhere. Tell everyone your stock is going to such-and-such a price. Deploy every available piece of good news, real or fabricated — big news can trap big institutions. Also, continuously pledge shares as collateral for loans, letting people see that you genuinely command massive capital, projecting an image of overwhelming strength. In reality, during distribution you don't need any push capital — just move your lips."

His words truly shocked me. I had never heard of this "talk-your-way-out distribution method" before.

I later shared this technique with a friend who was struggling to distribute because he lacked push capital. After deeply absorbing Li Biao's approach, my friend had an epiphany. He first had the listed company produce a major positive announcement (a strategic cooperation agreement with a famous university in internet technology — costing only 1 million yuan), then used this to successfully get several mutual funds to lock up shares. The fund lockup turned his stock into an internet tech darling, attracting abundant buying. The locked-up fund capital also freed up over 100 million in push capital. External buying plus new push capital — my friend quickly drove the price up, resolving an otherwise hopeless situation. A single small shift in thinking transformed what had been a dead position into a fully live game.

On the topic of distribution themes, Li Biao said: "Historically, the two themes that support market-making are concept stories (like the current internet tech craze) and price-illusion stories (like high bonus share dividends or rights issues). For distribution purposes, the price-illusion theme may be more important."

Indeed, during the market-maker era, all historical mega-bull stocks were those with consecutive high bonus share dividends that fully filled the gap. But when this illusion game was played too long, would investors fall for it forever?

Li Biao agreed, saying that when any game is played long enough, everyone figures out the trick and the game is ruined. "So," he said, "for a maker to succeed, one must keep innovating — creating new games. New games are unfamiliar to people, making them easier to draw in."

I said: "After years of market-making, all the tricks are known. What new game could possibly feel fresh to investors?"

At this point, Li Biao seemed to suddenly remember something and said: "Actually, there's a stock we're currently working on that represents exactly this kind of soon-to-be-extinct new game."

I asked: "There's such a thing? What stock?"

"Shenzhen Saige," he said.

After a moment's thought, I said: "That stock sounds familiar — isn't it about to do a large rights issue?"

He said: "Exactly. This high-ratio rights issue is the new game. Remember the three consecutive limit-downs on Zhongguancun last August?"

I certainly did. Zhongguancun was listed through a backdoor takeover of Qiong Minyuan. Before listing, it conducted a 10-for-10 rights issue to all holders. Due to different ex-rights price formulas between the Shenzhen and Shanghai exchanges, when institutional shareholders waived their rights, the Shenzhen formula produced an artificially inflated ex-rights price. This phenomenon was taken to its extreme with Zhongguancun...

[Li Biao then explained the detailed mechanics of exploiting the pricing discrepancy — using the artificially high ex-rights price to create three consecutive "phantom" limit-down days, which would then attract bottom-fishing buyers, effectively allowing the maker to sell at the pre-ex-rights peak price.]

After the thorough explanation, I understood — it was equivalent to selling at the absolute peak price of 35 yuan. As long as subsequent trading days maintained heavy volume around that level, the maker could exit their entire position near the peak.

Li Biao said: "So this 10-for-8 rights theme is actually better than 10-for-10 bonus shares — this is the real price illusion. Precisely speaking, it's a price delusion, wrong twice: first the ex-rights price delusion, then the three-limit-down delusion. This delusion is like an open pit trap — everyone can see it, yet no one can avoid falling in. Truly baffling."

I said: "Perhaps that's the bewitchment of the innovative game you described."

Li Biao said: "I expect this kind of game can't last long. Shenzhen Saige may well be the last of its kind."

Our conversation ran long. As we parted, Li Biao reminded me they would soon start pushing Shenzhen Saige — I could buy some at the current 20 yuan. I was deeply grateful for his sincerity.

Sure enough, within days, Shenzhen Saige began its ascent. In just 10 trading days, the price rose from 20 yuan to 33 yuan. The rights registration date was March 31, 2000; that day, the stock touched 36.5 yuan and closed at exactly 35 yuan — perhaps not a coincidence. In the three trading days after ex-rights, exactly as we'd discussed, the stock produced three consecutive gap-down "limit-down" days.

The slight deviation from our prediction: on the third limit-down day, buyers appeared, producing 4.6% turnover, but the limit-down wasn't broken. On the fourth day, the stock stopped falling at limit-down — dropping only 3%, but with 23% turnover. I knew Li Biao's team was distributing massively that day.

But to an outsider, the same market action could be interpreted differently. I knew the heavy volume on day four was maker distribution — untouchable. But uninformed investors likely thought: after three limit-downs, a short-term bounce was due; the heavy volume meant a major player was bottom-fishing; the stock should rise further. Driven by this psychology, buying flooded in. An open pit trap, yet people couldn't see it — rushing to jump in.

Over the following 10 trading days, the stock held above 20 yuan with 83% turnover. Li Biao's team should have been nearly fully exited. By my calculation, Li Biao's average exit price equated to about 32 yuan pre-ex-rights — selling at virtually the peak. In the 12 years since, even at the 2007 bull market peak, Shenzhen Saige's price never touched that level again. This shows how ruthlessly Li Biao's team operated. Li Biao was a fine person, but when trading, he was a cold-blooded killer.

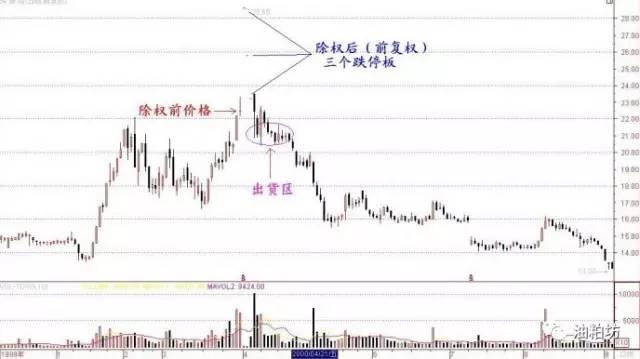

For a more intuitive impression, I've attached two charts of Shenzhen Saige's ex-rights: one unadjusted, one forward-adjusted:

- Unadjusted chart:

- Forward-adjusted chart:

Li Biao's team accumulated Shenzhen Saige from around 8–9 yuan and distributed everything at 32 yuan. Though the profit was only 1–2x, the money was earned with extraordinary ease. Shenzhen Saige's success came from brilliantly exploiting a regulatory loophole, exploiting human psychological weaknesses, and — most importantly — seizing with extraordinary sensitivity the opportunity the market presented.

To this day, I consider Shenzhen Saige the most brilliantly designed, most smoothly executed, and most perfectly concluded market-maker stock in history — achieving the highest realm of the market-maker era. Throughout the entire operation, the listed company published no false information, the maker used no deceptive chart techniques, and everything flowed naturally like floating clouds and running water, with no trace of the chisel. The run-up was perfectly calibrated — neither too hot nor too cold — all betraying the extraordinary skill of the operator.

A good market-maker stock should be relatively low-profile, not attracting excessive market attention, yet allowing the maker to earn handsomely — with no subsequent trouble. Regulators don't investigate, investors don't resent it, and it leaves no particularly strong impression — like a bird leaving no trace in the sky. Shenzhen Saige achieved all of this.

In September 2000, I met Li Biao one more time. He was truly a busy man. After exiting Yi'an Technology and Shenzhen Saige, he immediately plunged into the trading of Shen'anda (000004, now Guonong Technology). In this meeting, we mainly discussed our outlook on the market ahead. Due to length constraints, I won't elaborate here.

Though I only met Li Biao three times, the impression and influence he left on me were profound. Before meeting him, I'd encountered and dealt with many market makers and large institutions — I'd seen my share of the world. But those makers and institutions all played by the book, operating in conventional, step-by-step fashion, all fighting the same kind of positional warfare — competing on capital and social resources. Li Biao was different. He took the road less traveled, operating with extraordinary flair, even a touch of the uncanny — like a light-footed master, fighting "decapitation strikes": deploying minimal resources for maximum effect.

Li Biao was a master of strategic design, skilled at architecting projects. He was also a master operator who had developed his own unique methods. To this day, I still haven't figured out where Li Biao learned all this. Could it truly have been self-taught?

It's entirely possible. After reading "Chan Zhong Shuo Chan," I learned that Li Biao's classical Chinese and classical poetry were remarkably accomplished. He even publicly challenged Kong Qingdong several times on The Analects and classical poetry. With such brilliance, self-enlightenment in stock trading is far from inconceivable. It's just a pity that Heaven envied his genius — at the very moment his life shone brightest, he drifted away.

I dedicate this essay to his memory.